What are the golden rules of accounting? Learn the fundamental principles that govern financial transactions and bookkeeping.

Madison Business Services Ltd provide accounting services throughout Cheadle Hulme, Manchester and Cheshire. From the principles of debit and credit to maintaining accurate records, our expert insights break down the essential rules that ensure accurate and reliable financial reporting.

In the world of accounting, credits and debits play a crucial role, serving as the fundamental building blocks of financial transactions. Understanding the principles of debit and credit is essential before delving into the three golden rules of accounting.

Debits and Credits: The Foundation

Debits and credits are equal but opposite entries in accounting books, impacting the five core types of accounts:

- Assets: Resources owned by a business with economic value that can be converted into cash, such as land, equipment, cash, and vehicles.

- Expenses: Costs incurred during business operations, including wages and supplies.

- Liabilities: Amounts owed to another person or business, such as accounts payable.

- Equity: The difference between assets and liabilities.

- Income and Revenue: Cash earned from sales.

A debit is recorded on the left side of an account, increasing an asset or expense account while decreasing equity, liability, or revenue accounts. A credit is recorded on the right side of an account, increasing equity, liability, and revenue accounts while decreasing asset and expense accounts. Each transaction must have corresponding debits and credits.

Debit the Receiver and Credit the Giver

This principle applies to personal accounts, which pertain to individuals or organisations. When you receive something, debit the account; when you give something, credit the account. The rule ensures accurate record-keeping of personal transactions.

Debit What Comes In and Credit What Goes Out

For real accounts, also known as permanent accounts, this rule guides the recording of transactions. Real accounts, including asset, liability, and equity accounts, do not close at year-end; their balances carry over to the next accounting period. When something comes into the business (e.g., an asset), it is debited; when something goes out (e.g., an expense), it is credited.

Debit Expenses and Losses, Credit Income and Gains

The final rule pertains to nominal accounts, which are temporary and closed at the end of each accounting period. Nominal accounts include revenue, expense, gain, and loss accounts. When a business incurs an expense or loss, the account is debited. On the other hand, when recording income or gains, the account is credited.

By adhering to these golden rules of accounting, businesses ensure accurate and systematic recording of financial transactions, maintaining the integrity and reliability of their financial data.

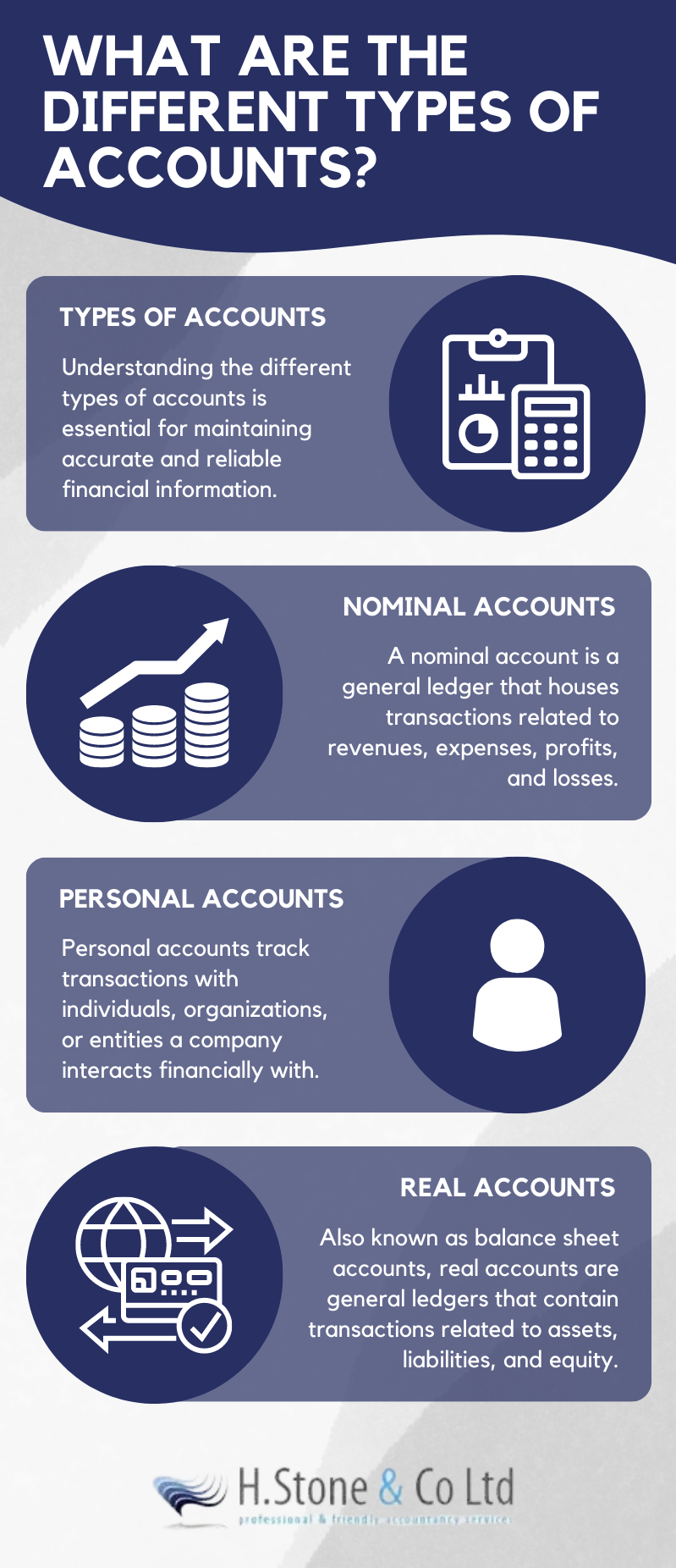

Types of Accounts

In the world of financial accounting, every debit or credit transaction is systematically recorded into various types of accounts. These accounts serve as the backbone of a company's financial records, helping to organise and categorise different types of transactions.

Understanding the different types of accounts is essential for maintaining accurate and reliable financial information. Let's explore the three primary types of accounts: nominal accounts, personal accounts, and real accounts.

Nominal Accounts

A nominal account, also known as an income statement account, is a general ledger that houses transactions related to revenues, expenses, profits, and losses. These accounts capture all the financial activities that occur during a particular fiscal year.

At the end of the fiscal year, these accounts are closed, and their balances are transferred to the company's retained earnings or profit and loss account. The balances are then reset to zero to begin the new fiscal year with a clean slate.

Nominal accounts play a vital role in determining a company's net income or net loss for a given period. By aggregating revenues and deducting expenses, businesses can assess their financial performance and make informed decisions. Examples of nominal accounts include:

- Revenue Accounts: Represent income generated from sales of goods or services, such as Sales Revenue or Commission Received.

- Expense Accounts: Encompass all the costs incurred during business operations, such as Wages, Rent, Utilities, and Office Supplies.

- Gain Accounts: Record profits earned from non-operational activities, such as the sale of non-inventory assets.

- Loss Accounts: Account for losses incurred from non-operational activities, like losses from the sale of assets or lawsuits.

Personal Accounts

Personal accounts are general ledgers that involve transactions related to individuals, organisations, or other entities with whom a company has financial dealings. These accounts are further categorised into three subcategories:

- Artificial Personal Accounts: Represent entities that are not human beings but are recognised as separate legal entities, such as banks, companies, partnerships, and government bodies. Transactions with these entities are recorded under their respective artificial personal accounts.

- Natural Personal Accounts: Deal with transactions related to human beings, such as individual customers (Debtors) who owe money to the company or suppliers (Creditors) to whom the company owes money.

- Representative Personal Accounts: These accounts represent the outstanding dues or advances due to or from individuals or entities for the previous or forthcoming fiscal year. For instance, the salary owed to an employee from the previous year or the rent paid in advance for the upcoming year would be recorded under representative personal accounts.

Real Accounts

Real accounts, also known as balance sheet accounts, are general ledgers that contain transactions related to assets, liabilities, and equity. These accounts focus on the company's financial position and help determine the net worth of the business.

Unlike nominal accounts, real accounts are not closed at the end of the fiscal year; instead, their balances are carried forward to the subsequent year.

Real accounts are further divided into two categories:

- Tangible Assets: These assets have a physical existence and can be seen and touched. Examples include land, buildings, machinery, equipment, vehicles, and inventory.

- Intangible Assets: Intangible assets lack physical substance but hold significant value to a company. Examples include patents, trademarks, copyrights, goodwill, and brand recognition.

Similarly, real accounts encompass both short-term and long-term liabilities, such as accounts payable, loans, and bonds. Moreover, they account for the company's equity, representing the residual interest in the assets after deducting liabilities.

Benefits of the Golden Rules of Accounting

Following the golden rules of accounting provides several benefits that contribute to the success and financial well-being of a business. These advantages ensure proper financial management, compliance with regulatory standards, and support decision-making processes.

One significant benefit is the proper maintenance of business records. Adhering to these rules ensures that financial transactions are accurately and systematically recorded, allowing for easy retrieval and facilitating well-informed decisions.

Another advantage is the ability to compare financial results over different accounting periods. Consistent and accurate recording of financial records enables businesses to analyse their financial performance, identify trends, and assess potential risks.

Properly calculating financial statements based on the golden rules assists in determining a business's valuation. Accurate financial data enhances credibility and attracts potential investors, supporting business expansion.

Furthermore, the golden rules of accounting facilitate budgeting and future projections. A sound budget, built on accurate financial data, provides a strong foundation for business growth and strategic planning.

In legal matters, well-maintained financial records serve as valuable evidence during disputes or lawsuits, protecting a company's interests.

Adhering to proper accounting practices also aids in tax-related matters. Accurate financial data ensures compliance with tax regulations, avoiding penalties and preserving the company's brand reputation.

Moreover, proper accounting is essential for achieving regulatory compliance. Regulatory authorities demand transparency and accuracy in financial reporting, and the golden rules help businesses meet these requirements, fostering trust with stakeholders.

In conclusion, following the golden rules of accounting has far-reaching benefits for businesses. From proper record-keeping to supporting decision-making and compliance, these rules establish a strong financial foundation, contributing to a company's long-term success and sustainability.

Get In Touch With our Tax Accountant Today

Are you looking for accounting services in Cheadle Hulme and the surrounding areas of Manchester and Cheshire?

Follow the link below for professional accounting near you.